While financial industry officials are literally sprinting to catch up with the many technological developments in the sphere, FinTech gives more and more beguiling promises of innovation every year, spawning a parallel universe of alternative financial services. Not to become an outsider in an “innovation marathon”, companies are actively investing in financial software development services, pushing the boundaries of the industry more every year.

In today’s article, we will shed light on top Fintech trends that are going to manifest themselves in 2022 and beyond.

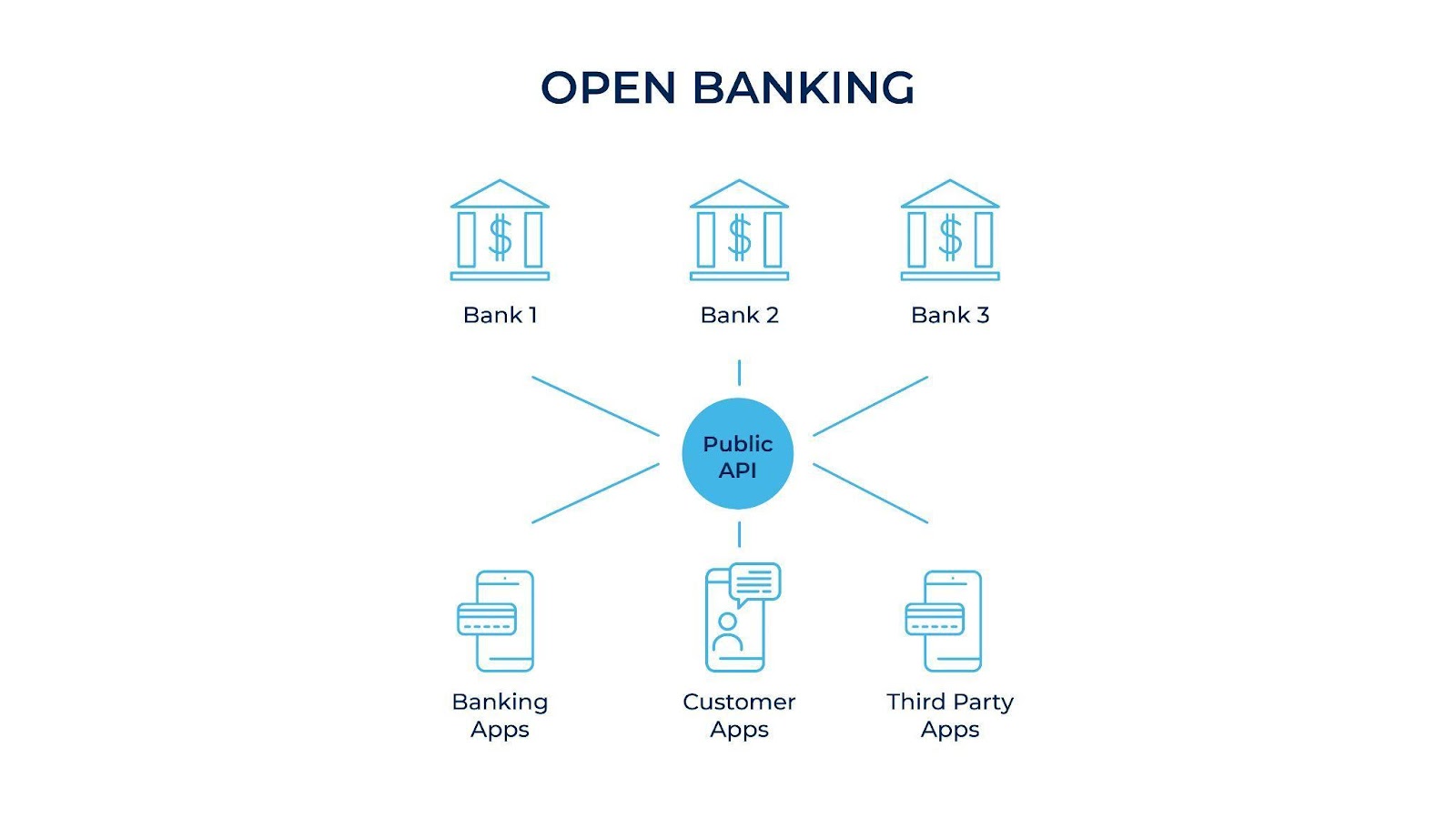

# Open Banking

Open banking is a fundamentally new approach to banking that is primarily aimed at improving competition, driving innovations, and offering customers more personalized and profitable services. The second Payment Services Directive, adopted in 2015, has become a legal basis for open banking and payment regulation within the EU, establishing new uniform standards and rules for transfers and payments.

According to PSD2, banks are obliged to exchange data with third parties such as FinTech companies, startups, etc., when it’s required by customers through Open API. Such an “openness” gives customers unlimited access to their data generated in a unified solution and more personalized and beneficial offerings from multiple service providers, while banks, in return, receive a chance to monetize the existing assets, enlarge new revenue streams, and foster innovation being a part of a large interdependent system. According to Accenture, 90% of financial chairmen state that open banking will increase organic growth by 10% in the near future.

In 2016, CMA (Competition and Market Authority) made the 9 biggest financial institutions in the UK open their APIs, transforming them from banks into financial service providers. The decision has totally changed the financial industry in the country, significantly simplifying the way how financial information is retrieved, shared, and presented.

# Smart Contracts

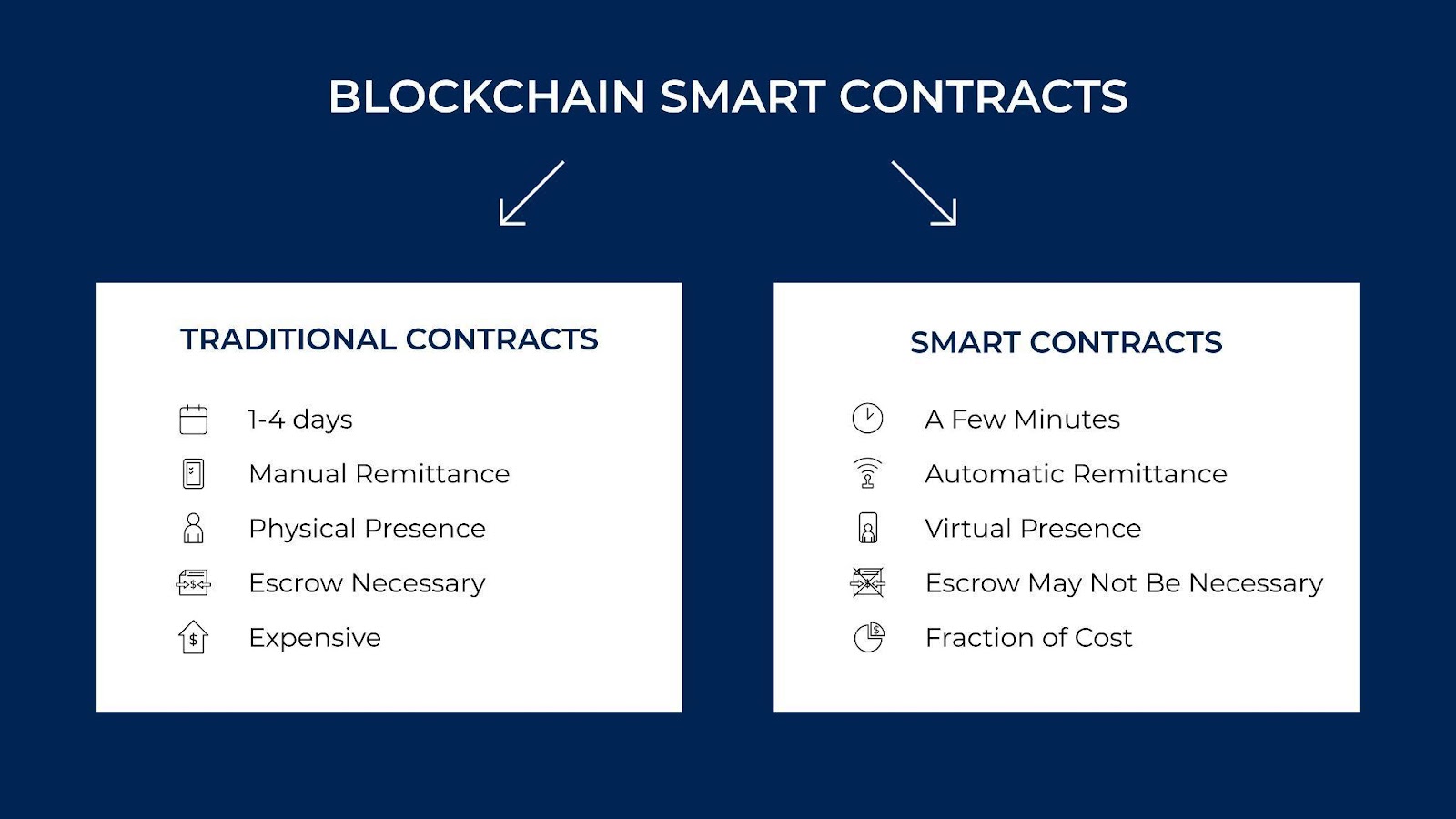

Blockchain-based smart contracts nowadays substitute traditional contracts which frequently require longer periods of time and bigger expenses. In the case with traditional contracts, there are two parties that sign identical copies of a paper agreement, while smart contracts streamline compliance through blockchain technology resulting in immediate and safe signing. With the help of blockchain, an executable code facilitates an agreement between two parties without the third party being involved. The code that embodies the readable terms of a contract, runs on the network which executes the actions as soon as predetermined conditions are met and verified. As soon as the transaction is accomplished, the blockchain is updated and the contract is initiated and irrevocable.

Without compromising on credibility, smart contracts ensure increased transparency within Fintech. By decentralizing the verification of contract terms, the partners become more liable towards each other, the contract negotiation process is simplified, and the parties cut down their expenses significantly.

# Decentralized Finance (DeFi)

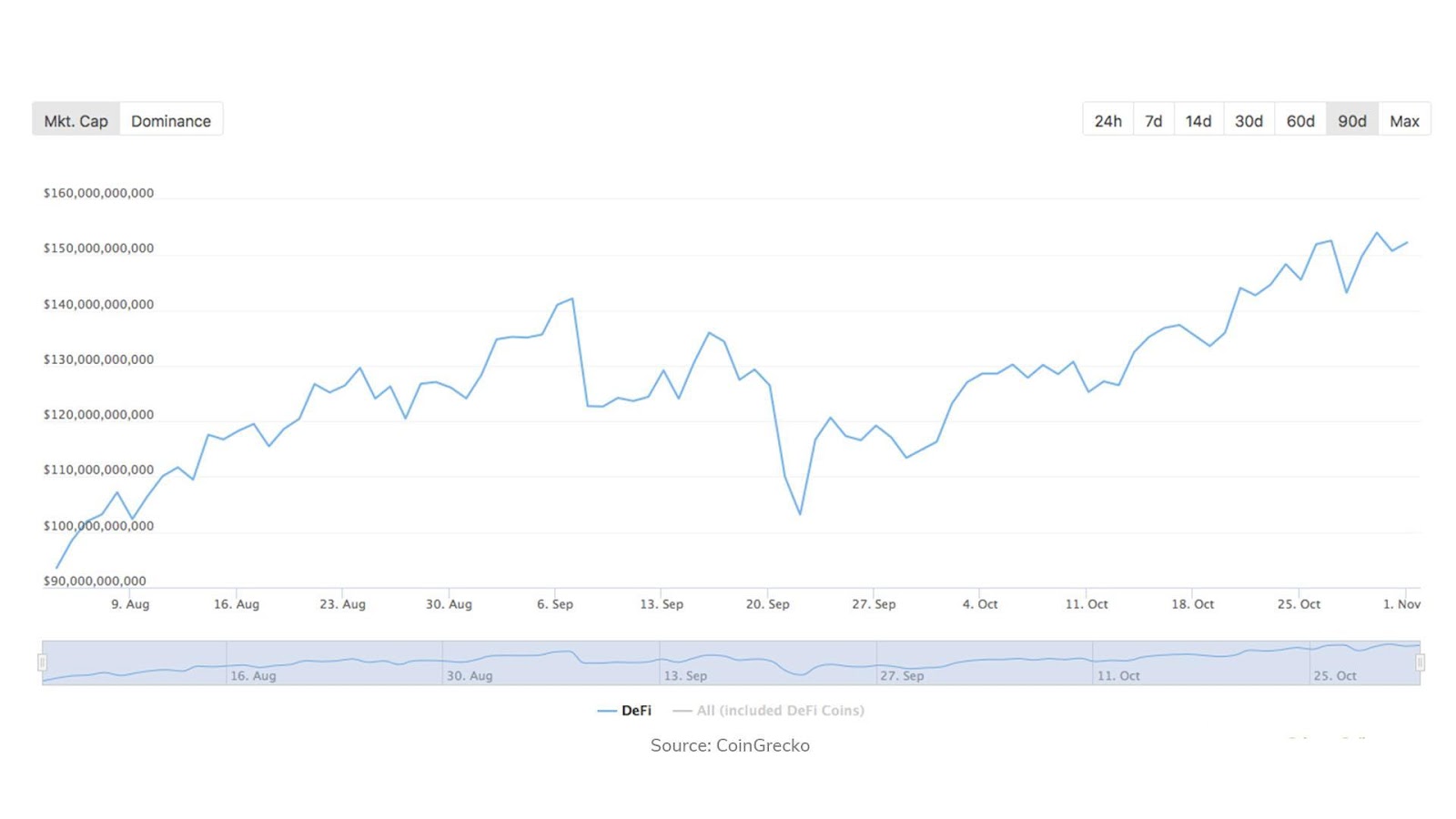

Decentralized finance is a blockchain-based form of finance that doesn’t depend on central financial intermediaries. Though it belongs to alternative financial tools and is associated with the crypto market, DeFi has seen massive growth recently and is predicted to expand more. In June 2021, there was $93 billion worth of DeFi assets in the crypto market, compared to $4 billion just three years ago.

A wide range of financial solutions such as exchanges, lending, and payment applications represent decentralized finance. The transactions are executed automatically through smart contracts on blockchains such as Etherum. DeFi allows any two parties to securely and at first hand transact without intermediaries or central authorities. Practically speaking, users don’t interact with a financial services company that collects their identifying information, or claims custody of their assets. It’s a completely computer-controlled market that innately executes transactions like issuing loans backed by cryptocurrency or paying interest on holdings. As a result, a much bigger number of people get access to financial services at lower costs and receive better interest rates in comparison to those offered by traditional financial institutions.

# WealthTech

Wealthtech refers to the usage of innovative technologies in investment management aiming at providing an efficient and automated alternative to traditional wealth management firms. As a result of growing regulatory responsibilities and compliance requirements, changing customer expectations and demands, and increased competition, Wealthtech has proven very popular over the past years. Robo-advisors are the most common “representatives” of Wealthtech. Through leveraging ML and algorithms, Robo-advisors are able to offer investment advice and management to their users, taking into account their investment opportunities, goals, income, risk aversion, and even marital status. According to Business Insider Intelligence, Robo-advisors will manage around $4,6 trillion by 2022. Among other examples of Wealthtech implementations are Robo-retirement (retirement savings accounts), digital brokerage (stock market information and investment opportunities), micro-investment (small investments without paying commission), etc.

Wealthtech has already disrupted the traditional understanding of finance and economy by promoting knowledge and efficiency in financial services and democratizing a range of activities that were exclusive to experts not so long ago.

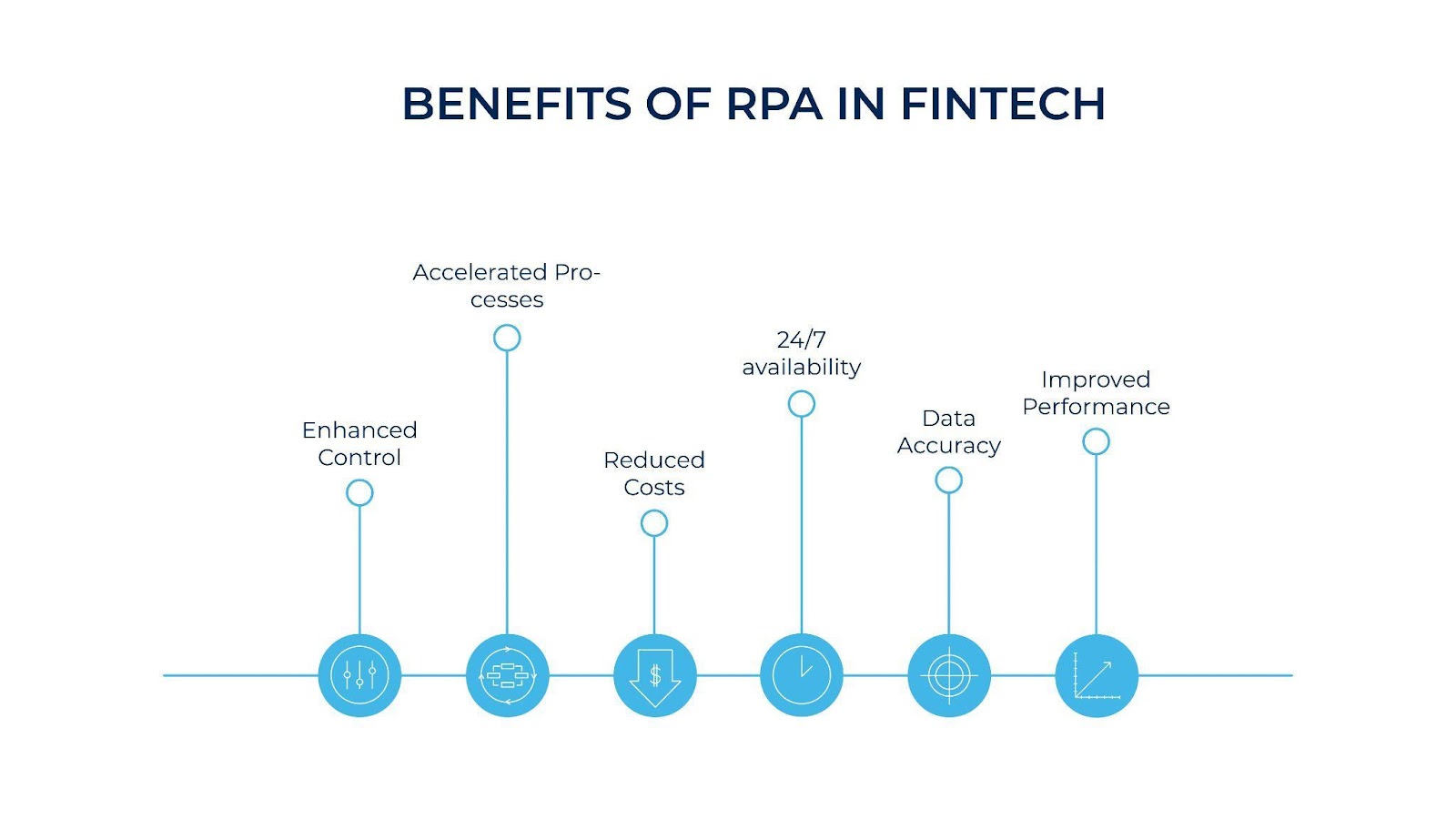

# Robotic Process Automation (RPA)

The expanding growth of RPA in financial services can be proven by the fact that the industry is estimated to reach $2,9 billion by 2022 which is a substantial increase compared to $250 million in 2016. Banks and financial institutions are actively investing in robotics to cut down on manual efforts, mitigate risks, ensure better compliance, and improve customer experience. RPA can be applied to a large number of financial operations such as customer onboarding, account opening, automatic report generation, mortgage lending, know your customer (KYC), and Anti-money laundering (AML). While virtual assistants take over these iterative human duties, employees can spend more time practicing their knowledge and performing more complicated and mission-critical tasks. The implementation of RPA solutions can save fintechs around 25-50% of processing time and cost.

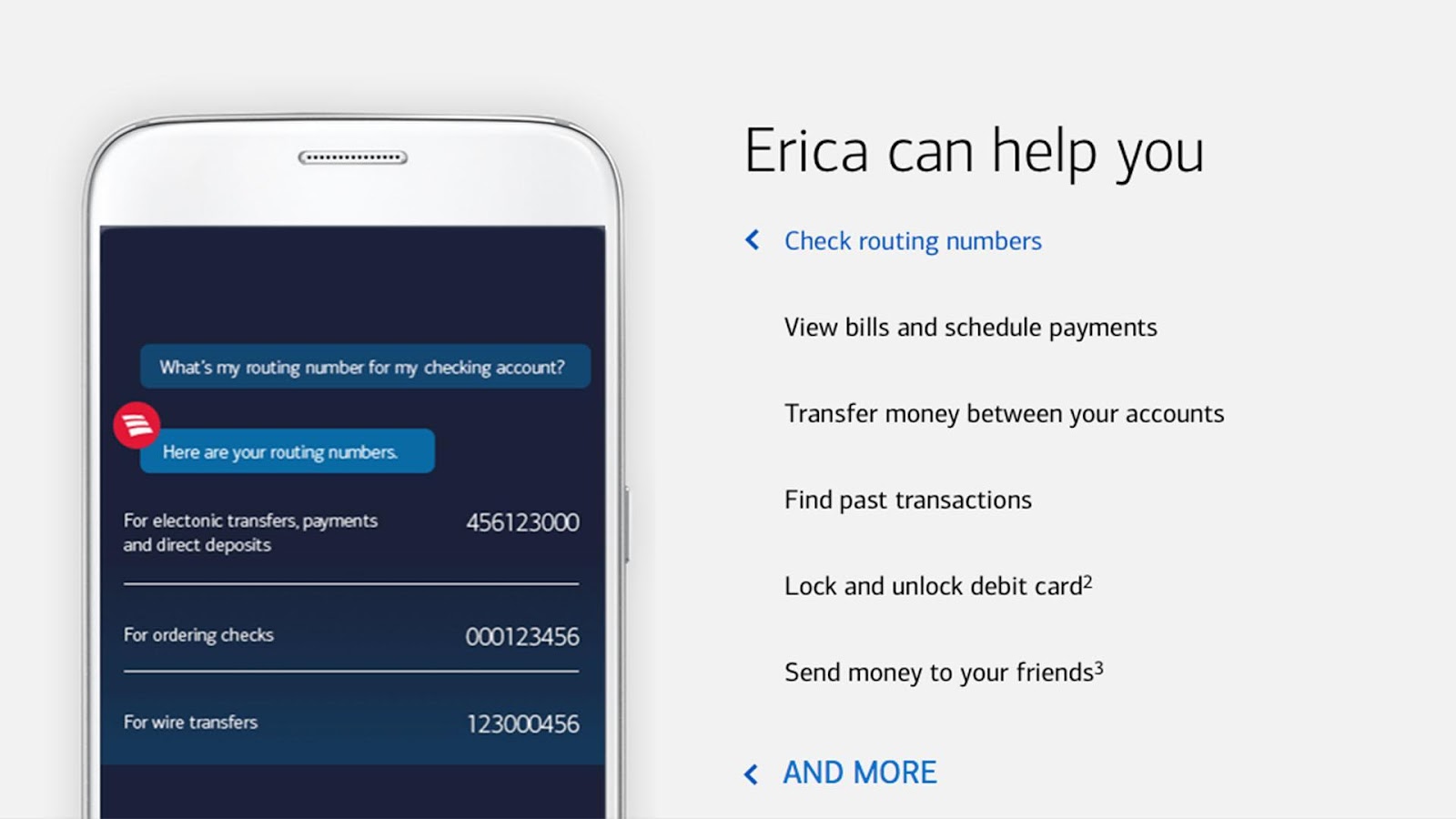

For example, Bank of America’s virtual assistant Erica is able to respond to more than a million financial questions. Leveraging ML, advanced analytics, and cognitive messages, the chatbot adapts to every conversation with a bank’s customer, shows transaction history, monitors recurring payments, and even reminds users to pay the bills.

Final Note

The technology has been brought to the forefront in the financial services industry with companies seeing a few years’ progress compressed into two or three months. People are turning “digital” in their mindsets and actions at an extremely fast pace. They want to make payments and transactions, invest money, and get loans as swiftly as possible. Therefore, in 2022 we’ll continue experiencing more automation, decentralization, and AI-based advisors and assistants available 24/7 in our pockets.